In April 2026, Cheniere Energy (LNG) stands as the primary beneficiary of a structurally tighter global energy market. Trading near $257.78, the stock is attempting to regain its momentum after touching an all-time high of $300.89 earlier this year. While the broader energy sector has been rocked by the U.S.-Iran conflict, Cheniere’s take-or-pay contract model, covering over 95% of its capacity, has transformed the stock into a utility-plus fortress for institutional investors.

As the market anticipates the Q1 2026 earnings release on May 7, the narrative is shifting from pure infrastructure growth to Capital Allocation Mastery. With a massive $10 billion share repurchase program underway and European gas storage at 5-year lows, Cheniere is at a crossroads. This guide breaks down the Cheniere Energy price prediction for 2026 using data from Goldman Sachs, JPMorgan, Morgan Stanley, and Zacks Investment Research.

You will also discover how to trade Cheniere Energy (LNG) stock futures with USDT through BingX TradFi.

Top 5 Things for Cheniere Energy (LNG) Investors to Know in 2026

- The $10 Billion Buyback: Cheniere’s board has authorized a massive repurchase plan to retire up to 21.1% of outstanding shares, providing a significant floor for the stock price.

- Middle East Supply Chaos: The ongoing Iran war has disrupted Qatari LNG exports, forcing European and Asian buyers toward secure, long-term U.S. contracts, specifically benefiting the Gulf Coast terminals.

- The $30 DCF Goal: Management is targeting a run-rate Distributable Cash Flow (DCF) of $30 per share, a metric that analysts believe could trigger a massive valuation re-rating.

- Expansion Catalyst: Investors are laser-focused on the Sabine Pass Stage 5 expansion and Corpus Christi Stage 3 progress. Execution here is key to meeting 2027 production targets.

- Institutional Dominance: With 87.26% institutional ownership, LNG is a conviction play for major funds seeking a hedge against geopolitical volatility and inflation.

What Is Cheniere Energy (LNG)?

Cheniere Energy, Inc. is the largest producer of liquefied natural gas in the United States and the second-largest operator globally. Headquartered in Houston, Texas, it sits at the heart of the global LNG trade, operating massive export terminals at Sabine Pass and Corpus Christi.

The company acts as a bridge between low-cost North American natural gas and high-demand international markets. Unlike traditional oil companies, Cheniere functions more like a toll road, collecting fixed fees for liquefying and transporting gas. As of April 2026, the stock trades at a forward P/E of roughly 10.4x, a valuation that Goldman Sachs and Citi describe as attractive given its 26.1% projected earnings growth for the year.

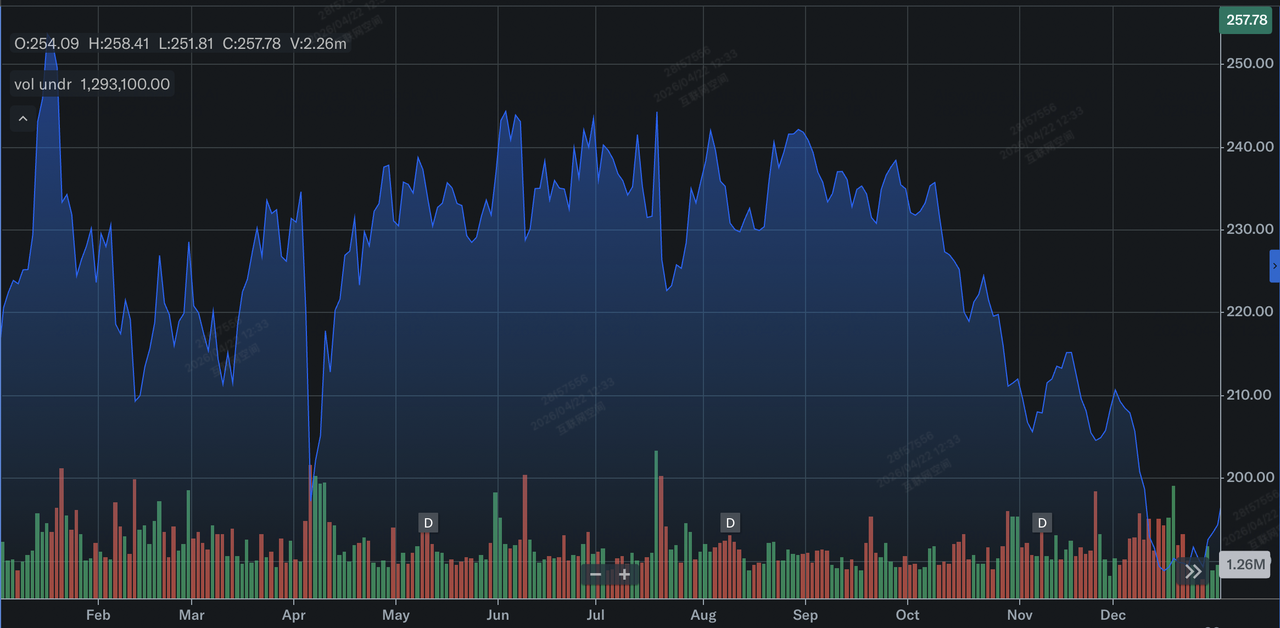

A Review of Cheniere Energy's Performance in 2025

Cheniere Energy (LNG) stock performance in 2025 | Source: Yahoo Finance

In 2025, Cheniere delivered a record-breaking performance, exporting 670 LNG cargoes and generating $19.97 billion in revenue, a 27% year-over-year increase. The defining theme of 2025 was the Energy Security Supercycle, as European nations permanently pivoted away from Russian pipeline gas in favor of U.S. LNG.

The company ended 2025 with $2.3 billion in Q4 net income, shattering consensus estimates and setting the stage for the aggressive capital return strategy we see today. This financial strength allowed Cheniere to de-leverage significantly, earning credit rating upgrades that lowered its cost of capital for future expansions.

Cheniere Energy's 2026 Strategy: Navigating Geopolitical Volatility

- Contracted Certainty: With over 95% of capacity tied to long-term agreements through 2030, Cheniere is largely insulated from daily fluctuations in natural gas spot prices.

- The Sovereign Shift: New 25-year deals with Taiwan’s CPC and Thailand’s utilities ensure that the company’s cash flows remain Better than the volatile spot market.

- Technical Support: Analysts identify the 200-day moving average at $224 as the line in the sand. As long as LNG stays above this level, the long-term bullish trend remains intact.

Cheniere Energy 2026 Investment Outlook: $330 Bull Run vs. $210 Bear Case

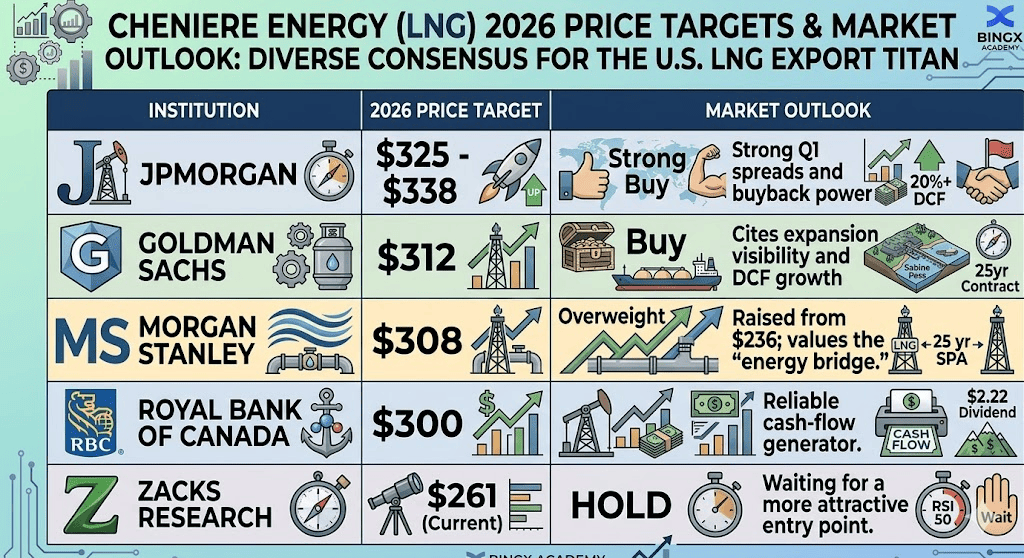

2026 prediction for Cheniergy Energy (LNG) stock by Wall Street analysts

To navigate the current energy landscape, investors must weigh these three distinct probability-weighted outcomes for LNG stock.

The Bull Case: The $330 Sovereign Security Breakout

The bullish narrative is anchored by a structural shift in the global supply-demand balance, specifically the Qatar Disruption resulting from prolonged friction in the Strait of Hormuz. As Qatari vessels face redirection or delays, JKM (Asian) and TTF (European) spot premiums are projected to surge. While 95% of Cheniere’s capacity is locked in, the remaining 5% uncontracted volume acts as a high-beta profit engine. In this scenario, these merchant cargoes could capture spreads exceeding $15–$20/MMBtu, providing a massive windfall that complements the company's steady take-or-pay revenue.

Practically, this case is amplified by the aggressive $10 billion share repurchase program, which is designed to retire approximately 21.1% of outstanding shares. As the share count shrinks toward the 175 million mark, the Distributable Cash Flow (DCF) per share is expected to accelerate toward a $30 run-rate. This combination of expanding spot margins and a tightening equity float creates the fundamental pressure needed to clear the $300 psychological resistance, aligning with top-tier price targets from JPMorgan for $338 and Wells Fargo for $335.

The Base Case: $280 – $295 Range-Bound Growth for Cheniere Energy

The base case defines Cheniere as a Quality Infrastructure Compounder, where value is driven by operational consistency rather than geopolitical spikes. The focus here is on the May 7th Q1 2026 earnings call, where management is expected to reiterate a robust Consolidated Adjusted EBITDA guidance of $6.75 billion to $7.25 billion. With European storage levels entering 2026 at five-year lows of roughly 140 cargoes below normal, demand for Cheniere's reliable U.S. supply remains high, supporting a steady recovery from the April pullback toward the analyst mean target of $293.

Investors should view this as a valuation catch-up phase. While the stock currently trades at a forward P/E of around 10.4x, a move toward its Fair Ratio of 18.33x, as suggested by Simply Wall St models, indicates significant intrinsic value remains. This scenario assumes the Corpus Christi Stage 3 project stays on schedule, with Trains 6 and 7 moving toward substantial completion. For traders, this translates to a low-volatility grind where the $233 50-day moving average serves as a reliable entry floor for a move toward the upper $200s.

The Bear Case: LNG Stock's $210 Infrastructure Trap

The bear case centers on a macro-skunk scenario: a sudden diplomatic breakthrough in the Middle East that leads to an immediate cooling of global energy premiums. If the geopolitical risk premium evaporates, the call on U.S. LNG may soften, leading to a contraction in spot margins that impacts Cheniere’s portfolio optimization earnings. Furthermore, any renewal of the federal LNG export permit pause or localized construction bottlenecks at the Sabine Pass Stage 5 expansion could trigger a sentiment shift from growth leader to stalled infrastructure.

Technically, this downside risk is marked by a decisive breach of the $230 support level, which would likely activate systematic selling programs. A move toward $210 would represent a retest of the 200-day moving average and a reversion to a Hold status, as suggested by Zacks Investment Research. In this environment, the company's debt-to-equity ratio of 1.74 becomes a focal point for bears, especially if interest rates remain higher-for-longer, increasing the cost of carry for its multi-billion dollar brownfield expansions.

Cheniere Energy (LNG) Price Forecasts for 2026 By Wall Street Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

JPMorgan |

$325 - $338 |

Overweight: Strong Q1 spreads and buyback power. |

|

Goldman Sachs |

$312 |

Buy: Cites expansion visibility and DCF growth. |

|

Morgan Stanley |

$308 |

Overweight: Raised from $236; values the "energy bridge." |

|

Royal Bank of Canada |

$300 |

Outperform: Reliable cash-flow generator. |

|

Zacks Research |

$261 (Current) |

Hold: Waiting for a more attractive entry point. |

How to Trade Cheniere Energy (LNG) on BingX

LNG/USDT perpetuals on the BingX futures market

Navigate the energy volatility of 2026 using BingX TradFi tools. Whether you are betting on a Q1 earnings beat or hedging against a correction in energy prices, BingX offers high-liquidity tools to access U.S. equities, powered by BingX AI analysis.

- Navigate to BingX TradFi and select Stocks.

- Search for LNG/USDT perpetual contract on the BingX futures market.

- Analyze the RSI and Moving Averages to identify entry points.

- Select Open Long if you expect geopolitical tailwinds to drive prices higher, or Open Short to hedge against a de-escalation in the Middle East.

- Set Take-Profit (TP) and Stop-Loss (SL) based on key resistance and support levels.

Top 5 Risks to Watch for LNG Investors in 2026

While Cheniere Energy maintains a dominant market position, investors must navigate a complex landscape of regulatory, geopolitical, and operational hurdles that could impact its 2026 valuation.

- Regulatory Fog: Shifts in U.S. Department of Energy (DOE) permitting for new export terminals.

- Construction Inflation: Rising labor and material costs for the Sabine Pass expansion.

- Geopolitical De-escalation: A sudden drop in global gas premiums if Middle East peace is achieved.

- Interest Rate Sensitivity: High debt-to-equity ratio of 1.74 makes the Cheniere Energy stock sensitive to higher-for-longer Fed policy.

- Spot Price Cooling: A global natural gas glut could impact the margins on Cheniere’s uncontracted cargo.

Final Thoughts: Is Cheniere Energy Stock a Good Buy in 2026?

Cheniere Energy in 2026 is the ultimate barometer of global energy stability. At $257, the stock trades at a discount to its intrinsic DCF value of around $393 per Simply Wall St. For long-term investors, the transition to a shareholder-return powerhouse makes it a compelling Buy. However, for tactical traders, the May 7th earnings report will be the decisive moment. Until the LNG stock reclaims $275, expect energy-driven swings.

Risk Reminder: Trading energy equities involves high volatility and exposure to geopolitical events. Cheniere Energy is sensitive to global gas spreads and U.S. regulatory shifts. Always perform your own due diligence and use risk management tools.

Related Reading

- Exxon Mobil (XOM) Price Prediction 2026: $180 Energy Alpha or Geopolitical Value Trap?

- Nasdaq 100 (NAS100) Forecast 2026: 27,000 AI Breakthrough or 22,000 Stagflation Trap?

- S&P 500 Forecast 2026: 7,600 Bull Run or a 6,000 Energy-Driven Crash?

- Crude Oil Price Forecast 2026: $140 War Premium or $60 Surplus Baseline?

- Is Gold a Good Investment in 2026? Risks & Returns Explained