Between July 2024 and June 2025, Brazilian investors transacted approximately $318.8 billion in digital assets, accounting for nearly a third of all crypto activity in Latin America. While the volume itself is massive, the underlying driver is even more telling: according to Chainalysis, stablecoins represent 90% of all digital asset activity in Brazil in 2025, fueled by the demand for fast, low-cost cross-border payments and domestic settlements.

This indicates that the vast majority of Brazilian crypto users are not speculating on Bitcoin or altcoins—they are holding digital dollars. However, leaving USDT and USDC idle in a wallet yields zero returns. Investors who know how to put these stablecoins to work can generate yields that outperform many traditional fixed-income products, all while retaining exposure to USD stability.

Quick Take: Generating passive income with stablecoins means earning interest on your USDT or USDC while maintaining a 1:1 peg to the US dollar. The main strategies include: (1) Flexible savings on exchanges with instant withdrawals, (2) Fixed-term savings for higher APY, (3) Lending on DeFi protocols like Aave, and (4) Structured products like Dual Investment. Typical yields range from 3% to 15% APY, depending on the strategy and risk profile.

What Are Stablecoins and Why Do They Yield Return?

A stablecoin is a cryptocurrency pegged to a stable asset, most commonly the US dollar. You do not "invest" in a stablecoin like USDC expecting price appreciation; its target price is always $1. The goal is simply efficient access to digital greenbacks.

But if the price doesn't change, how do you earn a yield?

The yield is generated by third parties who need liquidity: traders borrowing capital to leverage positions, DeFi protocols requiring liquidity pools to operate, and CeFi platforms bridging this capital and distributing a portion of the interest back to depositors.

Think of it like a USD-denominated investment account. You deposit capital, third parties utilize it and pay interest, and you earn yield on your digital dollars while maintaining a stable $1.00 base value.

Yield-Bearing Stablecoins vs. Active Yield Strategies

There are two distinct paths to generating passive income with stablecoins:

Traditional stablecoins with active yield strategies (USDT, USDC): You hold standard stablecoins and manually deposit them into savings or lending products. The asset itself does not auto-compound; the yield depends entirely on the platform where it is deployed.

Yield-bearing stablecoins (Native Yield): Unlike standard stablecoins that sit idle in a wallet, yield-bearing stablecoins are natively designed to accrue value over time. The yield is built into the token mechanics, removing the need to manually stake, lend, or lock funds to earn APY. Examples include sDAI, Ethena's USDe, and Ondo Finance's USDY.

For most retail investors entering the market, the first option offers the most direct and accessible onboarding ramp.

How to Calculate Your Stablecoin Yield

Before deploying capital, understanding the underlying math helps manage expectations.

The benchmark metric is APY (Annual Percentage Yield), which calculates your annual return taking compound interest into account.

Basic Formula:

Estimated Annual Yield (USD) = Principal × APY

Practical Example:

If you deposit $2,000 in USDT at a 6% APY:

- Annual Yield: $2,000 × 0.06 = $120

- Average Monthly Yield: $120 ÷ 12 = $10 per month

With the USD/BRL exchange rate at R$ 5.80, that $10 monthly return equals roughly R$ 58/month, completely insulated from crypto asset price volatility.

Additionally, there is a macro benefit: by holding assets in USD, international investors protect their purchasing power against local currency depreciation. If the USD appreciates against the Brazilian Real over the year, the forex gains stack directly on top of your crypto APY.

Total Return Formula (Local Currency):

Total Return (BRL) = Principal (USD) × (1 + APY) × Ending FX Rate (BRL/USD) − Principal (USD) × Starting FX Rate (BRL/USD)

The 4 Main Strategies to Earn Passive Income with Stablecoins

1. Flexible Savings on Crypto Exchanges (CeFi)

The easiest entry point for beginners. You deposit USDT or USDC into an exchange, subscribe to a flexible savings product, and start accruing interest daily with no lock-up periods and instant liquidity.

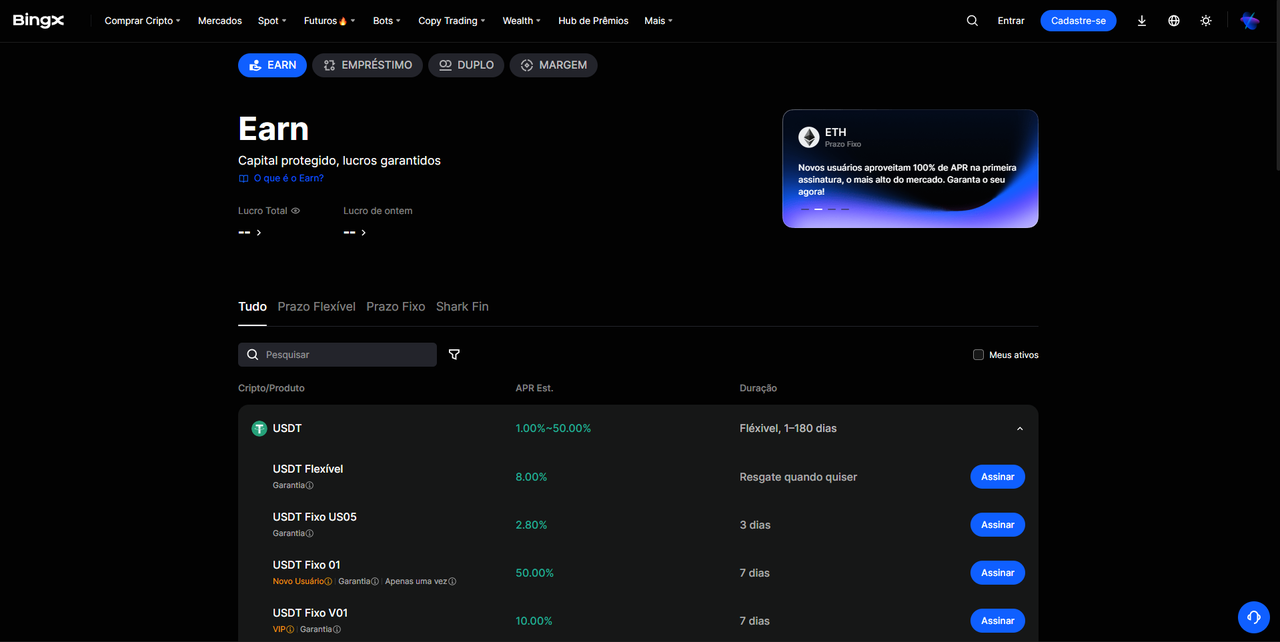

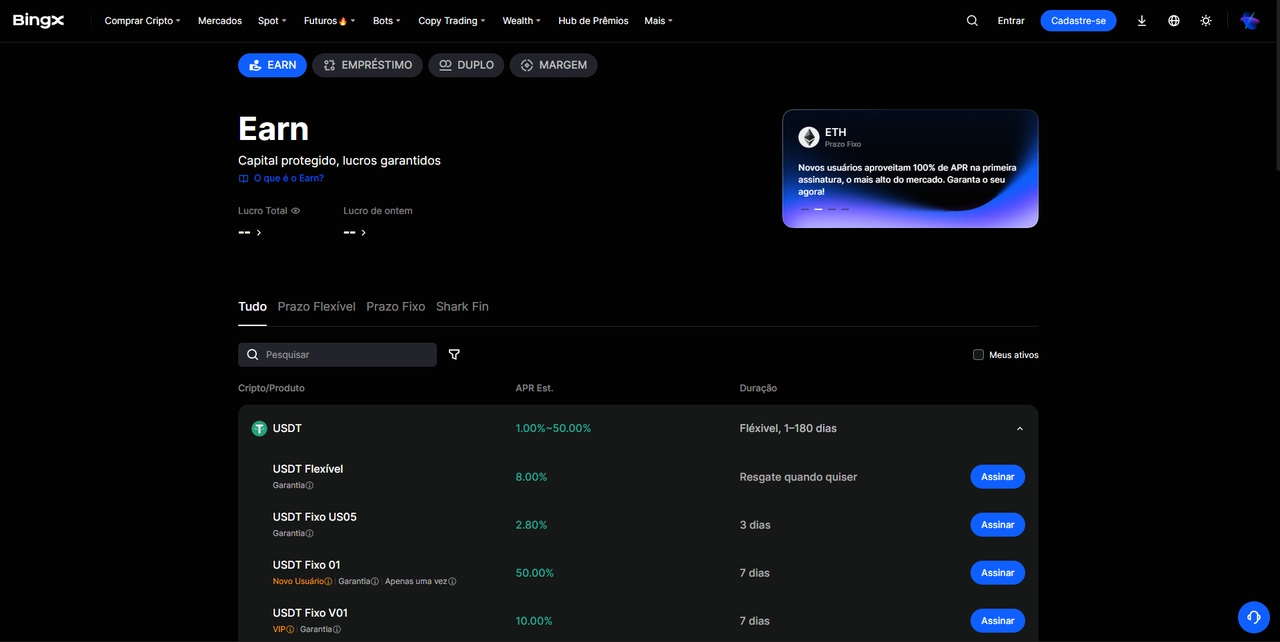

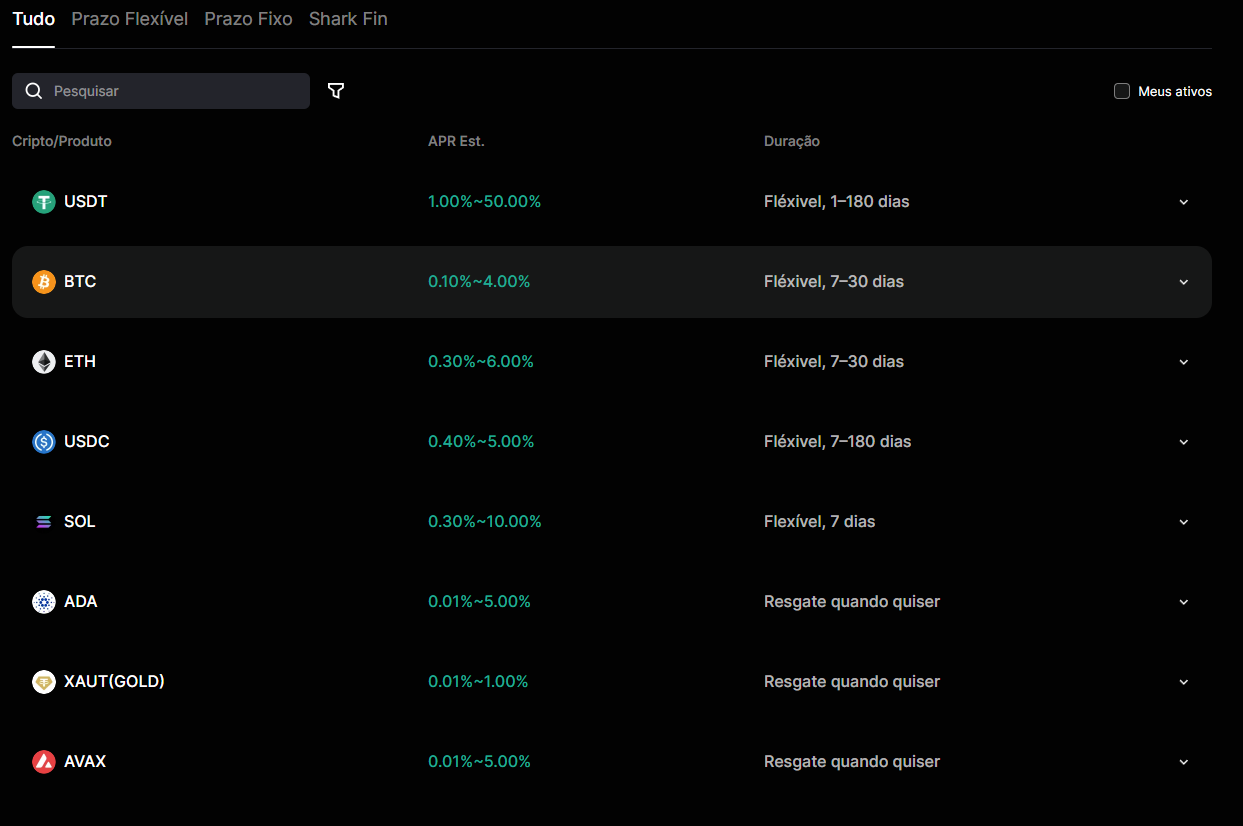

BingX Wealth is a comprehensive asset management service designed to put idle funds to work, generating consistent returns. The platform supports major cryptocurrencies including USDT, BTC, ETH, and more, offering both Flexible and Fixed-Term options to suit individual liquidity needs.

BingX’s Flexible Savings product allows users to redeem funds at any time with zero penalties or hidden subscription fees. Furthermore, BingX is among the leading exchanges implementing a Merkle-tree Proof of Reserves system, guaranteeing 100% backing for all user assets.

Best suited for: Investors who prioritize liquidity and want immediate access to capital. While flexible APYs are generally lower than fixed-term rates, they comfortably outperform traditional fiat savings accounts.

2. Fixed-Term Savings

By agreeing to lock up your capital for a specified period (7, 14, 30, or 90 days), you lock in a significantly higher APY. The logic mirrors traditional bank CDs: the more predictable the liquidity is for the platform, the higher the yield they offer you.

BingX features a USDT Earn product that enables users to generate passive income via stablecoin savings, with attractive APYs ranging from 1% to 15%. Fixed-term products typically land at the higher end of this bracket, especially during periods of high market demand for stablecoin liquidity.

Best suited for: Capital allocators with a fixed investment horizon who want to maximize yield without navigating DeFi complexities.

3. DeFi Lending Protocols

Decentralized lending connects stablecoin depositors directly with borrowers via smart contracts, cutting out the centralized middleman. Stable tokens like USDC and DAI yield average returns of 4% to 8% APY on top protocols with minimal volatility. Safety is secured through over-collateralization. To borrow USDC, a user must deposit a larger value of ETH or another liquid asset. If the collateral's value drops, the smart contract automatically liquidates it, mitigating default risk for depositors.

Platforms like Aave, Compound, and Morpho are industry standards. The process requires connecting a self-custody wallet like MetaMask, supplying the stablecoin to the lending pool, and receiving interest-bearing yield tokens. Interacting with these protocols requires a compatible Web3 wallet and an understanding of underlying network gas fees.

Best suited for: Crypto-native investors comfortable with Web3 infrastructure, non-custodial wallet management, and on-chain monitoring. The primary risk here isn't asset volatility, but rather smart contract risk—the vulnerability of the protocol code to exploits.

4. Structured Products: Dual Investment and Shark Fin

For investors looking to push beyond basic savings products without venturing into DeFi, centralized exchanges like BingX offer structured products. These instruments blend capital preservation with above-average yield potential.

BingX Shark Fin is a prime example. The product categorizes assets based on bullish or bearish market outlooks, offering four distinct options: Bullish_BTC, Bearish_BTC, Bullish_ETH, and Bearish_ETH. Depending on your market forecast, you select a direction and lock in a specific subscription price range. Upon maturity, if the underlying asset's price settles within your predefined target range, you unlock a higher tier APY. If the price breaks outside the range, you still walk away with a guaranteed base rate. Because the subscription asset is USDT, your principal remains fully protected against market volatility.

Best suited for: Investors with a clear directional view on BTC or ETH who want to boost their yield profile without risking their core principal.

What is the Real Return? Comparing Yield Strategies

|

Strategy |

Typical APY |

Liquidity |

Primary Risk |

Complexity |

|

Flexible Savings (CeFi) |

3%–6% |

Instant |

Exchange counterparty |

Low |

|

Fixed Savings (CeFi) |

5%–12% |

At maturity |

Exchange counterparty |

Low |

|

DeFi Lending (Aave, Morpho) |

4%–8% |

Variable |

Smart contract exploit |

Medium |

|

Shark Fin / Dual Investment |

6%–15%+ |

At maturity |

Counterparty + Market |

Medium |

|

Yield-Bearing Stablecoins |

4%–10% |

Variable |

Smart contract + Protocol mechanics |

Medium / High |

In 2026, the baseline for the best stablecoins for passive income ranges from 3% to 6% APY, with advanced strategies outperforming these figures under specific market conditions. Sustainable crypto yields are now largely anchored in real-world value (RWA), including tokenized US Treasuries, institutional lending desks, and delta-neutral basis trading.

As a rule of thumb, remain highly skeptical of any product promising consistent double-digit APYs without clearly disclosing the underlying mechanics of where that yield is generated.

How to Get Started on BingX: Step-by-Step

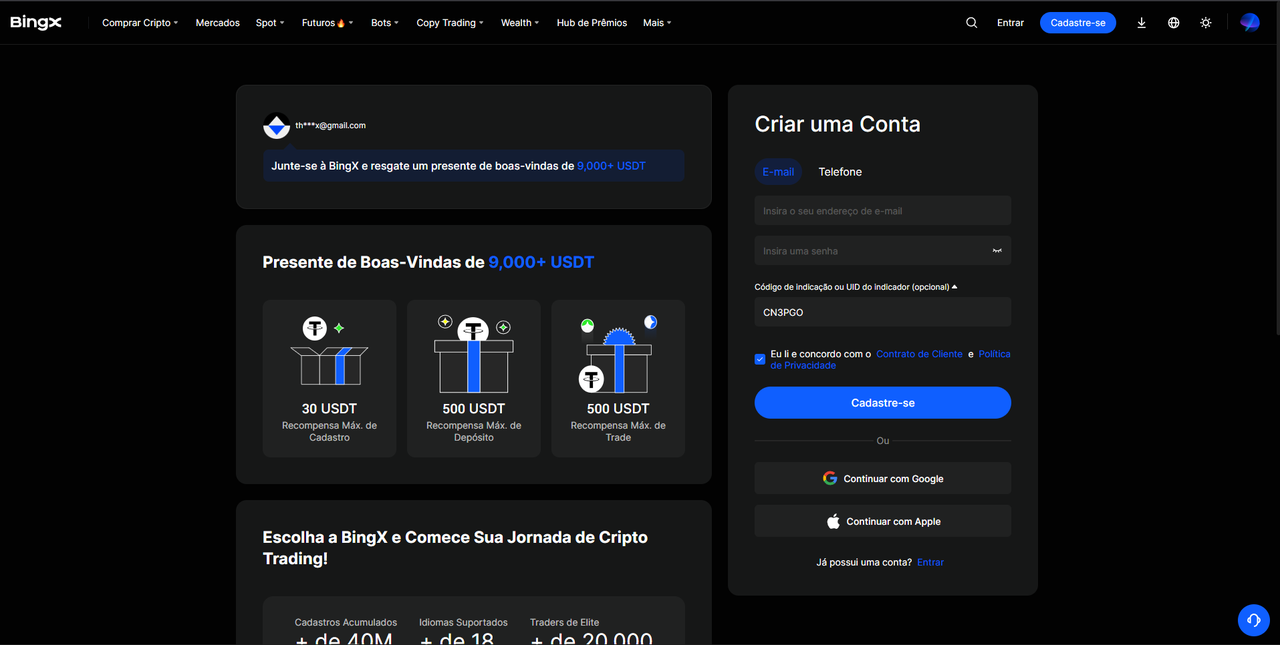

1. Create an Account and Complete KYC: Head over to bingx.com, sign up using your email or mobile number, and complete the identity verification (KYC) process. KYC is mandatory for deposits, withdrawals, and access to all Wealth products.

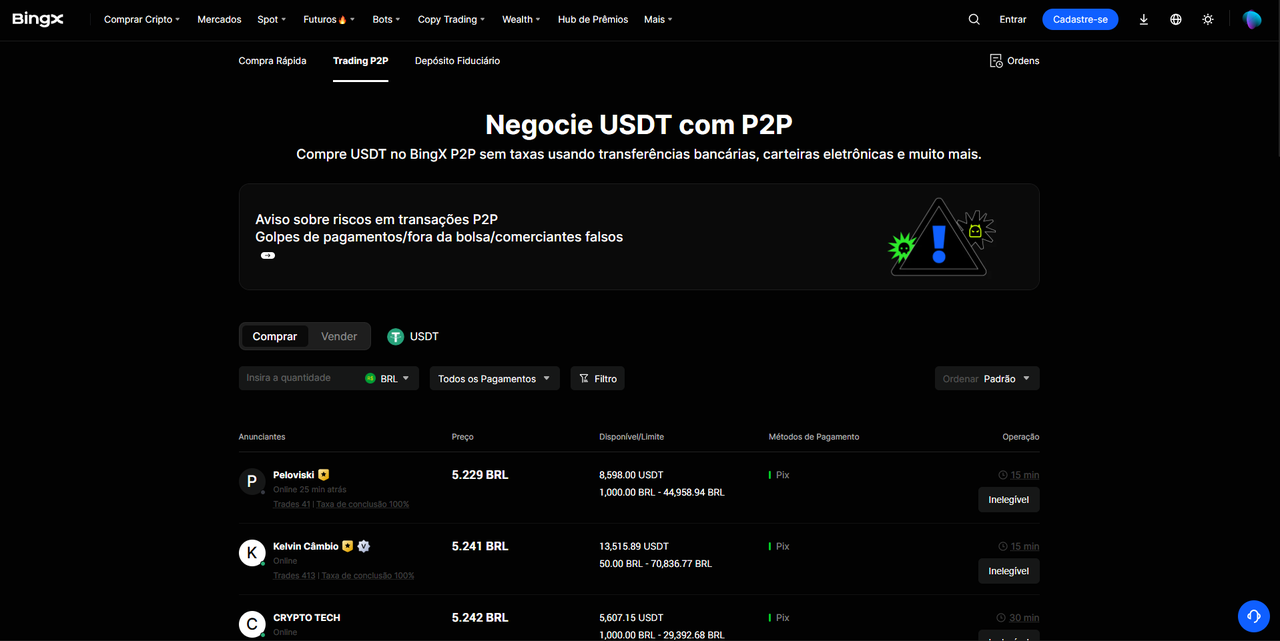

2. Deposit Fiat via P2P (e.g., PIX for Brazil): Navigate to the BingX P2P marketplace to buy USDT directly with your local fiat currency (such as Brazil's PIX system). This provides a seamless, friction-free way to onboard into stablecoins without heavy bank FX fees. Check out the fiat deposit tutorial if you need assistance.

3. Access the Wealth Dashboard: In the main navigation menu, click on the "Wealth" or "Earn" tab. Here, you will find all available interest-bearing products, including Flexible Savings, Fixed Savings, Shark Fin, and Dual Investment.

4. Select a Product Aligned with Your Profile: Just starting out? Opt for Flexible USDT Savings. Have a 30-day or longer horizon? Evaluate Fixed Savings. Have a strong directional view on BTC or ETH? Explore Shark Fin.

5. Subscribe and Monitor: Yield begins compounding according to the product parameters. For Flexible products, you can redeem at any time. For fixed-term structures, principal and accrued interest automatically credit to your account at maturity. Make sure to enable 2FA (Two-Factor Authentication) beforehand to secure your funds.

How to Declare Stablecoin Yields for Taxes (Brazil Market Focus)

Stablecoin yields are subject to local tax regulations. In Brazil, investors who hold crypto assets with an acquisition cost of R$ 5,000 or more as of December 31 must declare them under the "Bens e Direitos" (Assets and Rights) schedule, with stablecoins like USDT and USDC categorized under specific asset codes (Code 03).

For returns generated via staking or DeFi lending, taxpayers should declare an initial acquisition cost of zero. Yields earned through DeFi or staking are taxed either as capital gains or as income under the progressive tax table, depending on the nature of the transaction.

As a rule of thumb for retail individuals: monthly crypto sales below R$ 35,000 are exempt from capital gains tax but must still be disclosed. For monthly sales volume exceeding this threshold, tax rates start at 15%. Crypto rewards distributed as interest (e.g., paid out in USDT) must be registered with an acquisition cost of zero.

It is highly recommended to leverage dedicated crypto tax software or consult a specialized Web3 accountant to audit your transaction history. BingX provides exportable transaction reports to streamline this reporting process. For large-scale stablecoin allocations that you do not plan to use for active trading, consider moving them to a secure hardware wallet, keeping only operational capital on the exchange.

FAQ: Passive Income with Stablecoins

1. What is APY in stablecoins and how is it calculated?

APY (Annual Percentage Yield) represents your real rate of return over a year, accounting for compound interest. If you deposit $1,000 at a 6% APY, you will hold approximately $1,060 after 12 months. Unlike simple APR (Annual Percentage Rate), APY factors in the compounding effect of interest-on-interest, offering a more precise metric for comparing yields.

2. Which stablecoin offers higher yields: USDT or USDC?

In practice, the APY variance between USDT and USDC is minimal across major platforms. USDT commands slightly higher liquidity on centralized venues, occasionally driving higher lending rates during periods of intensive leverage demand. Conversely, USDC is often preferred by risk-averse institutions prioritizing regulatory compliance and asset-backing transparency, backed by Circle's public, audited reserves.

3. Do stablecoins earn interest automatically just sitting in a wallet?

No. Traditional stablecoins like USDT and USDC are static assets. You must manually deploy them into a CeFi savings product or a DeFi lending protocol to begin capturing interest. The exception lies in native yield-bearing stablecoins (like sDAI or USDe) which accrue value directly within the token contract, though these introduce additional layer smart contract complexities.

4. Is it safe to hold USDT on an exchange like BingX?

Exchanges featuring fully audited, Merkle-tree Proof of Reserves provide significantly higher structural transparency. However, counterparty risk is inherent to any centralized venue. Because of this, institutional and retail allocators frequently split capital—utilizing trusted exchanges for yield generation and migrating long-term holdings to self-custody cold wallets.

5. Are stablecoin yields taxed?

Yes. In most jurisdictions, rewards received from lending, savings, or DeFi are treated as taxable events. For example, under Brazilian rules, received tokens enter your balance sheets with a zero-cost basis, and capital gains tax applies if total monthly sales cross the R$ 35,000 threshold. Always consult a local crypto-native tax professional to maintain compliance.

6. What is the difference between flexible and fixed savings?

Flexible savings allows for instant deposits and withdrawals at any time, typically offering a lower, variable APY. Fixed savings locks up capital for a predetermined duration (e.g., 30 to 90 days) in exchange for a premium, fixed interest rate. The mechanism mirrors traditional banking deposit certificates: the more predictable the liquidity is for the platform, the better the yield for the depositor.

7. What is impermanent loss and does it impact stablecoins?

Impermanent loss (IL) is a risk unique to Automated Market Maker (AMM) liquidity pools in DeFi, occurring when the price ratio of two pooled assets diverges after deposit. For stablecoin-only pools (like USDT/USDC on Curve), IL risk is practically negligible because both assets maintain a tight 1:1 dollar peg. It only becomes a critical factor if you provide liquidity to mixed pools containing a stablecoin paired with a volatile asset like BTC or ETH.

Key Takeaways

- Stablecoins do not yield returns on their own. They must be actively deployed into savings, lending, or DeFi ecosystems to generate passive income.

- Sustainable baseline yields in 2026 range between 3% and 8% APY for risk-managed strategies, with structured products pushing past 12% via fixed timelines.

- BingX provides three explicit entry routes for USDT passive income: Flexible Savings (instant liquidity), Fixed Savings (higher yield via lockups), and Shark Fin (principal-protected structured products).

- Emerging markets like Brazil show massive structural demand, where stablecoins capture 90% of all crypto transaction volume due to local fiat integration (PIX) and global dollar onboarding.

- All accrued crypto yields must be properly managed for tax filings. Earned interest enters with a zero-acquisition cost basis and is subject to local capital gains rules.

- Exercise caution with double-digit APYs that lack clear revenue transparency. In 2026, sustainable on-chain yields are driven by real economic utility, including RWA tokenization and delta-neutral cash-and-carry strategies.

Related Articles

- Best Stablecoins to Invest in Brazil 2026: The Complete Guide

- PIX and Crypto in Brazil: Why Stablecoins (USDT and USDC) Dominate in 2026

- Beginner's Guide to Stablecoins and How They Work (2026)

- Understanding 6 Different Types of Stablecoins: A 2026 Breakdown

- What Are the Best and Most Popular Stablecoins for Your Wallet in 2026?