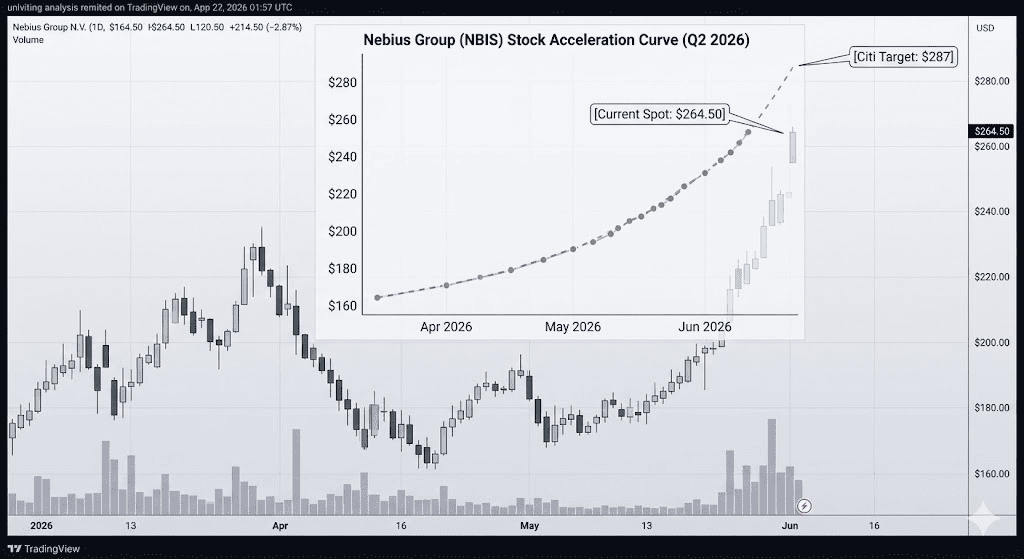

In early June 2026, Nebius Group (NBIS) stands at the epicenter of the global artificial intelligence infrastructure frenzy. Following a vertical rally supercharged by a 5.6% passive stake disclosure from Leopold Aschenbrenner's prominent hedge fund, Situational Awareness, the Amsterdam-headquartered neocloud provider is currently trading near $264.50, a staggering 221% surge year-to-date.

While the stock spent the early part of the year flying under the radar, back-to-back corporate breakthroughs have entirely redefined its narrative. Investors are now weighing a phenomenal first-quarter 2026 financial report against a massive capital expenditure ramp-up that is putting immense pressure on immediate margins.

As tech giants transition rapidly from general software toward agentic AI frameworks and automated machine learning clusters, the demand for raw GPU processing capacity has transformed specialized cloud builders like Nebius into high-conviction market darlings. With an order book heavily anchored by tier-one technology enterprises, the traditional valuation floor is being rapidly rewritten.

This guide breaks down the Nebius Group stock forecast and price prediction for the remainder of 2026, utilizing data from Citigroup, Wedbush, Goldman Sachs, and official regulatory disclosures.

You will also discover how to trade Nebius (NBIS) stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Nebius Group Traders to Know in 2026

As Nebius navigates a high-stakes environment of hyper-growth metrics and massive infrastructure financing, traders must monitor these five market-moving factors.

- The $50 Billion Hyperscaler Backlog: Nebius's order book features structural, multi-year contracts with mega-cap tech giants. This includes a massive $27 billion five-year contract with Meta Platforms and a $19.4 billion compute deal with Microsoft for dedicated AI capacity.

- The Nvidia Alliance: Beyond a core supplier relationship, Nvidia invested $2 billion directly into Nebius. During the COMPUTEX technology trade show in Taiwan, Nvidia CEO Jensen Huang explicitly praised Nebius as one of the world's premier world-class AI clouds.

- Aggressive Capacity Metrics: Management has aggressively pushed its year-end 2026 contracted power capacity target to over 4 GW. This expansion includes breaking ground on a gigawatt-scale AI factory in Independence, Missouri, and scaling its European data centers in Mäntsälä and Lappeenranta, Finland.

- The Capex vs. Profitability Dilemma: Nebius increased its full-year 2026 capital expenditure guidance to a range between $20 billion and $25 billion. While revenue is growing at a triple-digit pace, this heavy data center infrastructure spending means the firm will maintain a net adjusted loss in the near term.

- High-Margin Software Pivot: The company's $643 million acquisition of Eigen AI and the integration of Clarifai’s core team represent a deliberate shift from standard Infrastructure-as-a-Service (IaaS) to Platform-as-a-Service (PaaS), aimed at maximizing operating leverage through software-plus-infrastructure layers.

What Is Nebius Group (NBIS)?

Nebius Group N.V. is an Amsterdam-headquartered AI infrastructure company focused on building full-stack GPU clusters, cloud platforms, and specialized architecture for large-scale training and inference applications. Operating as a pure-play neocloud operator, Nebius competes head-to-head with modern infrastructure providers like CoreWeave to secure and deploy cutting-edge hardware solutions.

As of mid-2026, the company’s core business model is defined by vertical integration. By designing its high-performance compute centers from the ground up, Nebius optimizes the integration of advanced graphics processing units (GPUs) and solid-oxide fuel cell technology via a 328 MW partnership with Bloom Energy to drastically lower localized power costs and bypass traditional utility grid bottlenecks.

Nebius Group's Performance in Early 2026: The Post-Earnings Repricing

Visual representation of the NBIS structural breakout following Q1 earnings and institutional disclosures.

The company kicked off Q2 2026 by reporting standout first-quarter financial results. Revenue surged to $399 million, marking a 75% sequential expansion over the previous quarter and a 684% year-over-year increase. Driven almost entirely by its core AI Cloud unit, which captured 98% of total revenue, the performance comfortably beat consensus Wall Street expectations.

Crucially, the segment's adjusted EBITDA margin expanded from 24% to 45% in a single quarter, signaling substantial operating leverage and immense immediate pricing power. The market responded symmetrically, with the stock breaking out from its historical base to reach consecutive record closing highs.

Nebius Group's 2026 Trading Strategy: Navigating Volatility Multiples

- The $220 - $230 Support Base: Technical analysts view the $220–$230 window as a vital structural support floor, aligned with the asset's pre-breakout consolidation zone. As long as NBIS respects this level on weekly candle closes, the macroeconomic uptrend remains intact.

- Evaluating Price-to-Sales Multiples: Trading at 65x trailing sales, the stock carries a significant premium compared to the tech sector median. However, forward-looking models imply a sharply compressed multiple of roughly 14x forward sales, highlighting the critical role that backlog conversion plays in justifying current prices.

- Monitoring Insider Trajectory: Investors should keep a close eye on technical distribution patterns. Notable executive profit-taking, around $123.5 million over a rolling 90-day period, has occasionally created short-term resistance barriers near the all-time high boundaries of $274.80.

Nebius 2026 Investment Outlook: $287 Street-High Peak vs. $180 Overvaluation Mean Reversion

Investors navigating the rapid valuation adjustments of Nebius Group must balance structural de-risking against a premium multiples setup.

The Bull Case: NBIS's $287+ Hyperscaler Compute Monopoly

The bullish thesis, aggressively advocated by Citigroup and Wedbush’s Dan Ives, hinges on the industrial-scale fulfillment of pre-sold infrastructure. Championed by Citi's street-high price target upgrade to $287, this path assumes that insatiable global demand for advanced AI model training will allow Nebius to consistently command high physical premiums for its GPU allocations.

In this scenario, the company's capital expenditure is not a speculative risk, but an immediate revenue engine backed by legally binding contracts with Meta and Microsoft. Asset-backed financing structures secured against these massive backlogs are expected to minimize immediate liquidity crunches. If the company continues to safely transition customers onto its newly built high-margin software-plus-infrastructure layers, structural pricing power should easily carry the stock beyond the $287 threshold toward key psychological milestones.

The Base Case for NBIS Stock: $240 – $260 Consolidation Plateau

The base case envisions a healthy consolidation phase where the market matches the company’s hyper-growth trajectory against its ongoing infrastructure expenditures. While revenue remains on track to match full-year analyst estimates of $3.44 billion, sustained capital deployments will likely keep GAAP earnings per share in negative territory, averaging a projected loss of -$1.44 to -$1.70 for the full year.

For long-term participants, this setup favors a stable range-bound pattern punctuated by bumps around the upcoming August 6 quarterly earnings release. The narrative here transitions away from sudden momentum spikes toward steady milestone achievements, such as bringing online the 328 MW fuel cell deployment or activating new Nvidia HGX B300 clusters via its TD SYNNEX distribution partnership.

The Bear Case: The $180 Overvaluation Mean Reversion Trap

The bearish outlook, highlighted by more conservative Wall Street estimates and firms like D.A. Davidson, which recently moved to a Neutral rating, focuses squarely on severe valuation inflation and execution bottlenecks. If regional power access constraints, supply-chain delivery delays for cutting-edge hardware, or rising secondary infrastructure alternatives begin to slow data center deployment schedules, the company risks failing to hit its aggressive year-end target of $7 billion to $9 billion in Annual Recurring Revenue (ARR).

Technically, if a deceleration in sequential revenue occurs, the current multiple structure leaves the stock vulnerable to sharp drawdowns. A decisive break below the $210 line in the sand would invalidate the near-term bullish structure, triggering momentum unwinding as speculative capital rotates back to mature cash-generating assets, dragging the NBIS stock back down to retest its historical consensus price target average of $182.75.

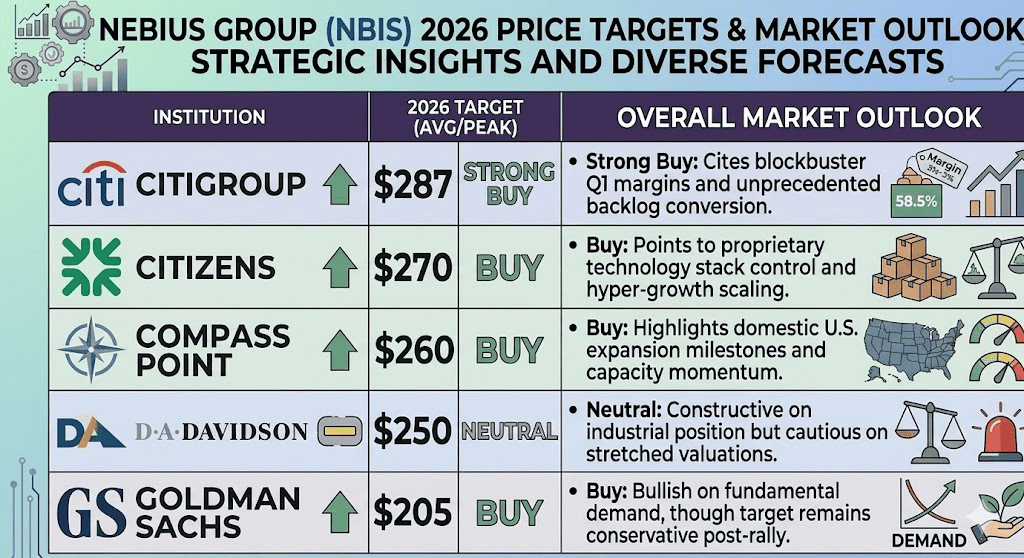

Nebius Group (NBIS) Price Forecasts for 2026 by Wall Street Analysts

|

Institution |

2026 Price Target (Peak/Avg) |

Overall Market Outlook |

|

Citigroup |

$287 |

Strong Buy: Cites blockbuster Q1 margins and unprecedented backlog conversion. |

|

Citizens |

$270 |

Buy: Points to proprietary technology stack control and hyper-growth scaling. |

|

Compass Point |

$260 |

Buy: Highlights domestic U.S. expansion milestones and capacity momentum. |

|

D.A. Davidson |

$250 |

Neutral: Constructive on industrial position but cautious on stretched valuations. |

|

Goldman Sachs |

$205 |

Buy: Bullish on fundamental demand, though target remains conservative post-rally. |

How to Trade Nebius Group (NBIS) Stock Futures on BingX TradFi

NBIS/USDT perpetuals on BingX futures market

As Nebius Group navigates this period of high-stakes infrastructure scaling and vertical price expansion, traders can seamlessly capitalize on its daily volatility through the BingX platform.

- Access BingX TradFi: Navigate to the specialized TradFi markets' portal on the main dashboard.

- Select Nebius Group (NBIS): Search for and select the NBIS-USDT perpetual futures contract.

- Choose Your Direction: Select Open Long if you anticipate the $50 billion hyperscaler backlog will drive shares toward the $287 street-high target, or select Open Short to trade the overvaluation mean-reversion setup.

- Select Leverage and Margin Mode: Apply your preferred isolated or cross-margin parameters alongside conservative leverage to optimize capital efficiency.

- Execute Risk Protocols: Utilize advanced BingX Take-Profit and Stop-Loss (TP/SL) tools to insulate your trading capital from abrupt, news-driven gap moves during extended market hours.

Top 5 Risks to Consider Before Investing in Nebius Stock

While the fundamental backdrop for this neocloud pioneer is supported by explosive institutional momentum, market participants must carefully weigh these high-impact headwinds.

- Severe Multiples Expansion: Trading at a steep 65x trailing sales, the stock carries a massive valuation premium that leaves it highly vulnerable to severe downside if subsequent growth metrics underperform.

- Massive Capital Burn: The company's aggressive full-year 2026 capital expenditure guidance of $20 billion to $25 billion puts substantial pressure on intermediate margins and delays near-term GAAP profitability.

- Aggressive Infrastructure Competition: Nebius operates in a highly capital-intensive space, competing directly against deeply entrenched, well-funded neocloud rivals like CoreWeave for market share and hardware allocation.

- Supply Chain and GPU Bottlenecks: Execution depends entirely on maintaining its deep alliance with Nvidia; any delays in the delivery of next-generation hardware clusters would severely stunt its projected ARR run-rate.

- Power and Grid Availability Constraints: Securing the massive amounts of electricity required to power its planned 4 GW capacity expansion leaves the firm exposed to regional energy inflation, utility bottlenecks, and localized infrastructure delays.

Final Thoughts: Is Nebius a Buy in 2026?

As of mid-2026, Nebius Group has successfully transitioned from a speculative cloud option into a high-visibility structural pillar of the broader AI hardware supply chain. At the $264.50 level, the equity market is actively pricing in highly visible revenue streams and a substantial institutional vote of confidence from leading ecosystem participants. For short-term tactical traders, structural momentum remains firmly in control as long as global macro support lines hold.

However, executing entries directly at all-time high extensions demands rigorous risk management. Long-term investors may find the most value by tracking localized consolidation periods near the base-case support lines, ensuring that entry parameters remain aligned with fundamental backlog delivery milestones rather than short-term momentum chasing.

Risk Reminder: Investing in high-growth technology infrastructure involves substantial capital risk due to elevated price volatility, heavy capital expenditure cycles, and intense competition within the cloud landscape. Always implement disciplined risk management and proper position sizing.

Related Reading

- Top AI Cloud Infrastructure Stocks to Buy in 2026 Amid Hyperscaler Capex and the Neocloud Boom

- Meta (META) Stock Price Prediction 2026: Can AI Efficiency and Custom Silicon Drive META to $900?

- Microsoft (MSFT) Stock Outlook for 2026: Can Azure AI and Copilot Growth Drive MSFT Stock to $550+?

- Top AI Hyperscaler Stocks to Watch in 2026: The $700 Billion Cloud Infrastructure Race

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?