Every May marks Taiwan's comprehensive income tax filing season. As the number of cryptocurrency investors continues to grow annually, "Do cryptocurrencies need to be declared for taxes?" has become one of the most pressing concerns for many crypto investors. For long-term holders, understanding the taxation logic of withdrawal timing is fundamental to asset allocation planning; for frequent traders, tax handling methods directly impact net returns and compliance risks. Cryptocurrency prices are highly volatile with considerable potential profits, but ignoring reporting obligations often results in tax authorities pursuing back taxes and penalties that exceed the original investment returns.

Taiwan has not yet established specific legislation for cryptocurrency taxation. The current practice classifies cryptocurrency trading profits as "capital gains income" under Article 14, Paragraph 1, Item 7 of the Income Tax Act. For beginners, the most common confusion involves not knowing which activities trigger taxation, how to distinguish between domestic and foreign income, and whether losses can be offset; for advanced users, considerations include anti-money laundering risks from large withdrawals, whether frequent trading might be classified as business operations, and future connectivity issues when crypto asset regulations are implemented.

This article starts with the legal positioning of cryptocurrencies, systematically explaining taxation timing, criteria for determining domestic versus foreign income, tax handling for various trading scenarios, reporting procedures, and introduces trading platforms and tax assistance tools suitable for Taiwan investors, helping you establish a stable and practical cryptocurrency tax reporting workflow. The content in this article is for general reference only; for actual reporting, please consult with accountants or tax authorities based on your personal circumstances for professional advice.

Key Takeaways

- Taiwan currently defines cryptocurrencies as "virtual commodities," with investment profits classified as "capital gains income" that must be reported under Article 14, Paragraph 1, Item 7 of the Income Tax Act, not eligible for the stock trading capital gains tax exemption.

- Taxation is triggered when "cryptocurrencies are converted to fiat currency and withdrawn to bank accounts." Holding or crypto-to-crypto exchanges within exchanges are unrealized gains/losses and do not immediately create tax obligations.

- Domestic versus foreign income is determined by the "withdrawal platform": withdrawals from Taiwan exchanges (MAX, BitoPro, etc.) are domestic income included in comprehensive income tax; wire transfers from overseas exchanges to Taiwan are foreign income subject to the Alternative Minimum Tax (AMT).

- Foreign income under NT$1 million per person annually is exempt from reporting. Amounts exceeding this must be reported for AMT, with other items added then minus the NT$7.5 million (applicable for 2026) exemption, with the difference taxed at 20% as minimum tax.

- BingX provides Traditional Chinese interface for spot and perpetual futures trading, with comprehensive profit/loss report export functions, suitable for Taiwan cryptocurrency investors as a primary trading and record-keeping platform.

Do You Need to Pay Crypto Tax in Taiwan? Rules and Legal Classification

Before understanding tax rules, it's important to grasp how Taiwan's regulatory authorities define cryptocurrencies legally. The Financial Supervisory Commission has issued multiple press releases since 2013, positioning cryptocurrencies as "virtual currencies" or "virtual commodities," not legal tender or financial products. This positioning directly determines taxation methods: cryptocurrencies are not eligible for stock trading capital gains tax exemptions, with investment profits treated as "income from sale or exchange of property and rights," similar to auctioning antiques or trading online game virtual items.

The Ministry of Finance submitted a written report on cryptocurrency taxation to the Legislative Yuan's Finance Committee in January 2025, further confirming that individual cryptocurrency trading profits should be reported as "capital gains income" under Article 14, Paragraph 1, Item 7 of the Income Tax Act, calculated as transaction proceeds minus costs and related expenses, then included in comprehensive income tax. As of December 13, 2024, tax authorities have identified NT$130 million in unreported virtual currency income, collecting over NT$34 million in back taxes and penalties, establishing actual enforcement precedents.

Tax law adopts the "exit settlement method" for calculating gains/losses, meaning gains/losses are only realized when cryptocurrencies are converted back to fiat currency (NT$ or foreign currency). In other words, if funds remain within exchanges, regardless of how much account values increase or exchanges between different tokens, no tax obligations arise. Only when cryptocurrencies are withdrawn to personal bank accounts and fiat conversion is completed does it need to be included in that year's income reporting.

How to Distinguish Domestic vs. Overseas Income: Based on Withdrawal Method

Determining whether cryptocurrency transactions constitute domestic or foreign income is the first step before calculating tax liabilities. Taiwan tax law treats these two categories very differently: domestic income is included in comprehensive income tax at progressive individual rates, while foreign income is subject to the Alternative Minimum Tax (AMT) with relatively lenient exemptions.

1. Domestic Income: Withdraw via Taiwan Exchanges

Using Taiwan-compliant exchanges like MAX and BitoPro to convert cryptocurrencies to NT$ and transfer to personal NT$ bank accounts classifies these profits as "domestic income" subject to individual comprehensive income tax regulations. Taiwan-compliant exchanges follow real-name system and anti-money laundering regulations with complete transaction records, allowing tax authorities to access specific individuals' trading data under Article 30 of the Tax Collection Act. Domestic income calculation is:

Domestic Capital Gains Income = Cryptocurrency Sale Amount - Purchase Cost - Trading Fees

The calculated income is included in annual comprehensive income totals, taxed at progressive rates (5% to 40%). For investors with modest profits, domestic income's lower-tier tax thresholds are relatively favorable; however, for high-income groups, the 40% progressive rate ceiling is significantly higher than foreign income's minimum tax system.

2. Overseas Income: Transfer Funds Back to Taiwan from Foreign Exchanges

If using overseas exchanges to trade cryptocurrencies and converting profits to USD or stablecoins before wire transferring to Taiwan foreign currency bank accounts, this income is considered "foreign income." Foreign income is not included in comprehensive income tax but is subject to the Income Basic Tax Act. When funds are remitted, banks require declaring the transfer nature; it's recommended to report "268 Sale of Foreign Virtual Assets" for future tax classification as foreign income.

Foreign income exemptions are relatively lenient. Annual foreign income under NT$1 million per person is exempt from reporting; amounts exceeding NT$1 million must be reported for AMT. After deducting NT$7.5 million (applicable for 2026) from basic income amount, the difference is calculated at 20% as basic tax. If basic tax exceeds comprehensive income tax, the difference must be paid; if comprehensive income tax equals or exceeds basic tax, no basic tax payment is required. Note that basic income amount includes not only foreign income but also specific insurance benefits, securities transaction income, etc., which should be considered when calculating exemption space.

Extended Reading:Complete Comparison of Taiwan Cryptocurrency Fiat On/Off Ramps: Which Platform Has the Cheapest Deposits and Fastest Withdrawals? (2026)

When Do You Pay Crypto Taxes in Taiwan? Common Scenarios

Different types of cryptocurrency transactions have slightly different tax treatments. Below are several common scenarios' tax determinations to help investors establish comprehensive tax awareness.

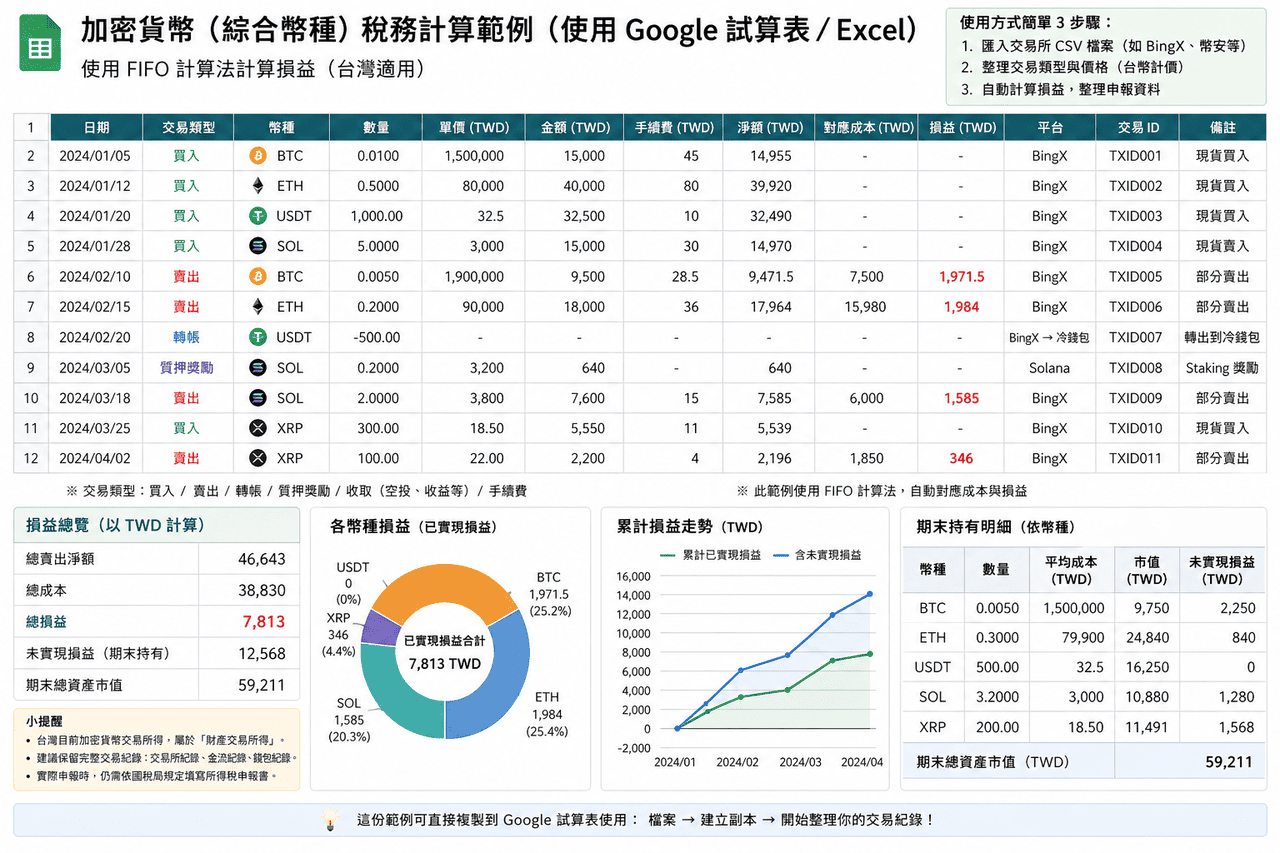

- Spot Trading Profit Withdrawals: The most common scenario involves buying cryptocurrencies, realizing profits after price increases, selling, and withdrawing to bank accounts. Such profits constitute capital gains income, classified as domestic or foreign income based on withdrawal channels. It's recommended to download complete trading records (including purchase time, price, quantity, and fees) as cost basis; for multiple purchases, FIFO or average cost methods can be used, but consistency should be maintained within the same year.

- Futures and Leverage Trading: Futures and leverage trading profits also constitute capital gains income. Due to mechanisms involving margin, funding rates, and forced liquidation, calculations differ from spot trading, with platform-provided profit/loss statements commonly used in practice. Trading through overseas platforms and remitting funds to Taiwan is typically classified as foreign income.

- Crypto-to-Crypto Exchanges: Converting one cryptocurrency to another within exchanges before fiat conversion is often considered unrealized gains/losses. Typically no immediate reporting is required, but trading records should be preserved for future cost basis calculations when withdrawing.

- Staking and Earn Rewards: Rewards obtained through exchange or on-chain protocolstaking currently lack clear tax guidance in Taiwan. Conservative approaches recognize rewards as income at market value when received; alternative approaches defer until withdrawal. Actual handling methods can be discussed with accountants based on circumstances.

- Airdrops and Mining Rewards: Airdrop tokens from projects ormining rewards are similar to receiving free property, potentially requiring market value recognition as income when received. Upon subsequent sale, the recognized market value serves as cost basis for calculating capital gains/losses.

- ArbitrageTradingand Frequent Trading: If individuals frequently engage in cryptocurrency trading at significant scales, they may be classified as business operations, requiring business registration and business tax payment. In Taiwan, individuals selling virtual commodities domestically with monthly sales reaching NT$80,000 need tax registration; those primarily engaged in cryptocurrency trading may be considered regular traders at NT$40,000 monthly sales.

Crypto Tax Rules by Transaction Type in Taiwan

|

Item |

Domestic Income |

Foreign Income |

|

Trigger Conditions |

Converting cryptocurrencies to NT$ through Taiwan exchanges and withdrawing |

Trading through overseas platforms and remitting funds to Taiwan in foreign currency |

|

Applicable Tax System |

Individual comprehensive income tax (capital gains income) |

Basic income amount (Alternative Minimum Tax) |

|

Tax Rate |

5% to 40% progressive rates |

Basic income amount exceeding NT$7.5 million applies 20% |

|

Reporting Threshold |

No threshold, any income requires reporting |

Foreign income under NT$1 million typically exempt from reporting |

|

Loss Offset |

Can report capital trading losses and carry forward for 3 years |

Requires complete supporting documents, practically difficult to recognize |

|

Audit Difficulty |

Centralized trading records, easier to organize and explain |

Scattered trading records, requires self-organization and verification |

Best Crypto Tax Tools for Taiwan Users

For Taiwan cryptocurrency investors with numerous transactions or multi-platform operations, manually organizing profit/loss data can be quite labor-intensive. The following tools can help integrate trading records and calculate gains/losses.

Most tools are international services with limited support for Taiwan tax systems, typically used mainly for calculating profit/loss figures. For actual reporting, data still needs to be reorganized according to Taiwan formats. Additionally, current mainstream tools are primarily English-based without complete Traditional Chinese support, requiring some adaptation during use.

- Koinly: Supports most mainstream exchanges and wallets, providing API and CSV import methods, automatically organizing trading records and categorizing as trades, transfers, fees, etc., reducing manual organization burden. Supports FIFO, LIFO, and average cost methods, generating profit/loss reports and tax summaries, suitable for users with numerous transactions or multi-platform operations.

- CoinTracker: Focuses on automatic synchronization and portfolio tracking, supporting most exchange API connections and CSV data import. The system automatically calculates holding costs and realized gains/losses, supporting FIFO and LIFO, suitable for users with relatively simple trading records or those wanting quick overall asset status insights. Free version has transaction limits; paid plans required as trading volume increases.

- Blockpit (formerly Accointing): Provides trading record integration, profit/loss calculation, and tax report functions, supporting FIFO and average cost methods. Former Accointing has been merged into Blockpit, continuing and integrating functions, suitable for medium trading volume scenarios. Outputs remain primarily international tax-focused, typically requiring reorganization for Taiwan reporting.

- Excel/Google Sheets: Independent of third-party tools, can directly import exchange CSV files, self-establish fields and calculation logic, completely organize data according to Taiwan reporting requirements. Suitable for users with modest transaction counts or those wanting complete calculation process control, offering advantages in format control and flexibility.

For Taiwan general investors with modest transaction counts (fewer than 50 transactions annually), using Excel or Google Sheets for self-organization is typically more practical than paid third-party tool subscriptions, as you can organize data completely according to Taiwan reporting format requirements without needing to convert tool outputs. High-volume or multi-chain operation advanced users can consider tools like Koinly to reduce organization workload, but still need to verify calculation accuracy themselves.

Crypto Tax Tool Comparison: Taiwan-Friendly Tools with Chinese Interface

|

Tool |

Traditional Chinese Interface |

Taiwan Tax Format |

BingX Import Support |

Supported Calculation Methods |

Cost |

|

Koinly |

No |

Partial Support (Can generate P&L reports) |

Manual CSV upload required |

FIFO, LIFO, Average Cost |

Free basic version, paid plans from ~$49 USD/year |

|

CoinTracker |

No |

Partial Support |

Manual CSV upload required |

FIFO, LIFO |

Free 25 transactions, paid plans from ~$59 USD/year |

|

Blockpit |

No |

Partial Support |

Manual CSV upload required |

FIFO, Average Cost |

Free basic version, paid plans from ~$79 USD/year |

|

Excel/Google Sheets |

Yes |

Complete Flexibility (Self-designed) |

Direct CSV import |

Customizable (FIFO, LIFO, Average Cost, etc.) |

Free |

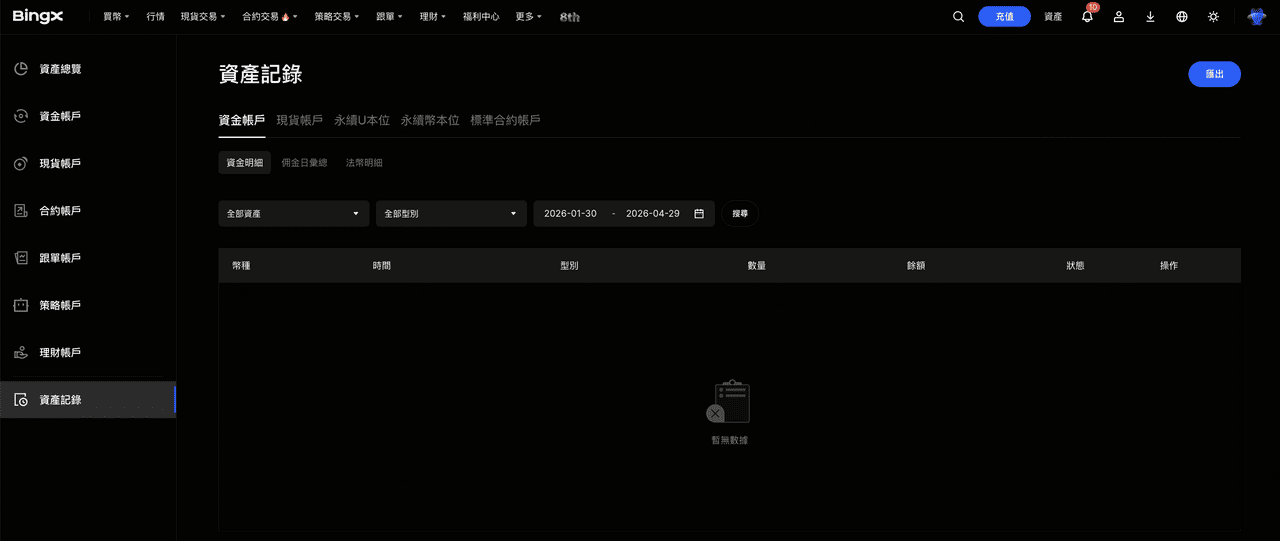

How to Export Trade History from BingX for Tax Filing

BingX's Traditional Chinese interface significantly simplifies record organization work before tax reporting. Below is the standard process for exporting complete cryptocurrency trading records from BingX, suitable for continuous daily record-keeping and annual tax organization.

- Log into BingX Account and Access Trading Records Page: After logging into BingX, go to "Assets" or "Orders" page to view complete account trading history. Includes spot trading, perpetual futures positions, and funding rate records.

- Select Export Time Range: On the trading records page, select "Export" function and set the current year's time range (January 1 to December 31). It's recommended to export quarterly as backup to avoid missing data when processing large amounts at year-end.

- Download CSV or Excel Reports: BingX supports exporting trading records as CSV or Excel formats, containing trading time, buy/sell direction, quantity, price, fees, and transaction amounts. This report can be directly used to calculate cryptocurrency capital gains income or imported into tools like Koinly for automatic processing.

- Organize Withdrawal Records: BingX's "Withdrawal History" page shows all withdrawals to external addresses or Taiwan exchanges. Align these records with bank-side remittance certificates as basis for determining domestic or foreign income.

- Backup to Personal Devices: Downloaded reports should be preserved for at least 7 years for potential future tax authority audits. It's recommended to backup to both personal computers and cloud services to avoid losing critical data due to single device failure.

5 Key Things to Know Before Filing Crypto Taxes in Taiwan

After understanding basic taxation principles, there are several easily overlooked details in practical operations that may directly impact reporting results and subsequent audit risks. Below are five key points.

- Cryptocurrency Trading Records Must be Actively Preserved: Taiwan exchanges currently don't mandate reporting users' annual asset details to tax authorities, and overseas exchanges are even less within Taiwan tax authorities' direct jurisdiction. Investors must download and preserve complete trading records, withdrawal certificates, and bank remittance proofs themselves. It's recommended to backup quarterly or annually to avoid losing critical data due to exchange policy changes or account anomalies.

- Crypto-to-Crypto Exchanges Don't Trigger Taxation, But Still Require Recording: Converting one cryptocurrency to another within exchanges hasn't realized gains/losses and doesn't immediately create tax obligations. However, when calculating cost basis for future withdrawals, you need to trace back to original fiat purchase costs. If multiple crypto-to-crypto exchanges occurred in between, complete trading records are key to reasonable cost calculation.

- Anti-Money Laundering Risks from Large Withdrawals: Single withdrawals exceeding NT$500,000 require banks to report to the Ministry of Justice's Investigation Bureau per regulations. However, amounts below NT$500,000 don't guarantee absolute safety; frequent deposits/withdrawals in short periods, abnormal amounts, or suspicious transaction patterns may still trigger bank risk controls. Maintaining stable withdrawal frequency and amounts while reducing abnormal transaction characteristics helps minimize the possibility of special attention.

- Foreign Income Exemption Isn't Fully NT$7.5 Million Available: Many investors mistakenly believe foreign cryptocurrency gains are tax-free as long as they don't exceed NT$7.5 million, but basic income amount includes other items such as specific insurance benefits, securities transaction income, non-cash donation amounts, etc. When planning tax strategies, first check how much exemption space other items have occupied, rather than judging solely based on cryptocurrency profit amounts.

- Legal Risks from Non-Reporting Exceed Back Tax Amounts: Failing to legally report cryptocurrency income not only faces back taxes but may also incur 15% annual late interest and 0.5 to 3 times penalties. If tax evasion amounts are large, criminal liability may even be involved. Honest reporting with complete record preservation is the most stable approach for long-term cryptocurrency market participation.

Conclusion: How to File Crypto Taxes in Taiwan

While Taiwan lacks specific cryptocurrency legislation, existing tax law can already tax virtual assets, with practical reporting and auditing gradually increasing. For investors, understanding basic taxation principles, distinguishing domestic versus foreign income sources, and preserving complete and traceable trading records are important foundations for long-term market participation. Rather than concentrating organization efforts before tax season, it's better to establish consistent recording methods during daily trading, such as regularly downloading trading data, unifying cost calculation methods, and completely recording each transaction and fee, making subsequent profit/loss calculation and reporting more substantiated.

In terms of tools and processes, a practical approach is task division by purpose: trading platforms provide original transaction and fund flow data, third-party tools help organize multi-platform or on-chain operations, and spreadsheets are used for final organization and checking according to Taiwan reporting formats. Through this structure, you can maintain efficiency while making data more complete and consistent; for larger trading scales or multiple operation scenarios, early discussions with professionals familiar with crypto assets can incorporate tax organization into daily management rather than concentrating efforts before tax season.

Related Reading

- Which Platform Has the Lowest Fees for Buying Bitcoin in Taiwan? BTC Price Spreads, Fees, and Liquidity Comparison (2026)

- Complete Comparison and Recommendations for Taiwan Cryptocurrency Futures Trading Platforms (2026): Fees, Liquidity, and Security Comparison

- Complete Comparison of Taiwan Cryptocurrency Fiat On/Off Ramps: Which Platform Has the Cheapest Deposits and Fastest Withdrawals? (2026)

- Taiwan Cryptocurrency Exchange Comprehensive Review: Beginner Registration Bonuses, VIP Rates, and Chinese Customer Service Complete Comparison (2026)

- Taiwan Exchanges vs. International Exchanges: How to Choose the Right Cryptocurrency Trading Platform for You?